Private equity investment and CPOM-compliant structures have made physician practice management fees more complex to design and defend. To comply with Corporate Practice of Medicine (CPOM) laws and physician fee-splitting prohibitions, management arrangements must be supported by fair market value (FMV). This article explains how physician practice management services are structured and how to determine fair market value for those fees.

Private Equity Deals Drive Management Arrangements

The recent wave of private equity investments in specialty physician practices has grown substantially over the past 10 years from primarily dermatology, gastroenterology, ophthalmology, and orthopedic specialty practices to also include vascular surgery and primary care, among other specialties. CPOM states are challenging for for-profit corporate operators, like private equity firms, that would prefer physicians to be employees, rather than independent contractors.

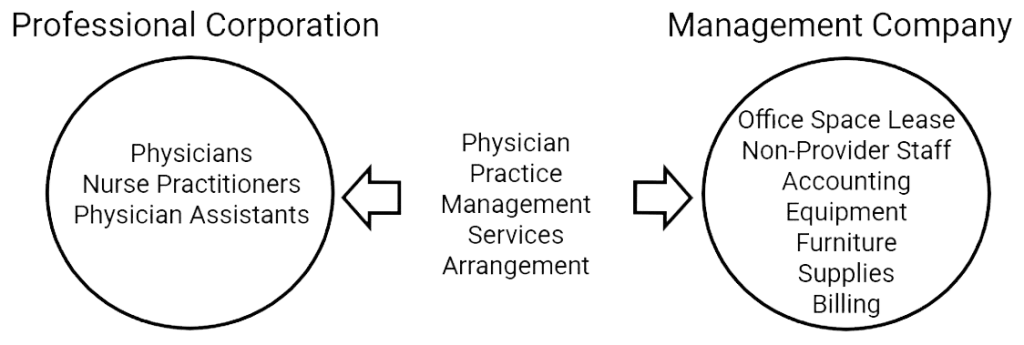

The CPOM restrictions are especially difficult to navigate when a physician practice wants to sell to a private equity firm. In these situations, the practices are limited to selling their tangible and intangible assets to the private equity firm’s management company and carving the medical and surgical professionals out of the deal into separate independent professional corporations that merely contract with the management company. The management company effectively holds the assets, office leases, and non-professional support staff of the practice, while the licensed physicians and advanced practice providers are employed by a separate professional corporation that contracts with the management company for comprehensive practice management services.

Structuring physician practice management arrangements in CPOM states requires careful alignment between operational design and fair market value. Early valuation input can help avoid compliance issues later in the transaction process.

Two Ways to Structure Physician Practice Management Services and Fees

To comply with CPOM laws and physician fee-splitting prohibitions, these arrangements usually require management fee rates to be set in advance. They also may require fees be fixed rather than use a standard percentage of revenues or collections rate, as is prevalent in management service arrangements.

There are two main ways to structure physician practice management services and fees:

À La Carte Physician Practice Management Services

À la carte physician practice management services let independent physician practices pick and choose what services they want from a menu. This model works well for management service organizations that want to align with independent physician practices, i.e., those that might not be ready or interested in complete practice management outsourcing.

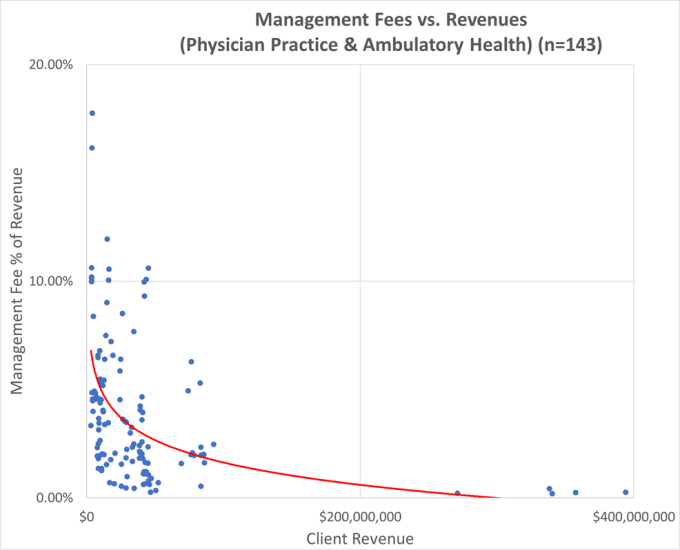

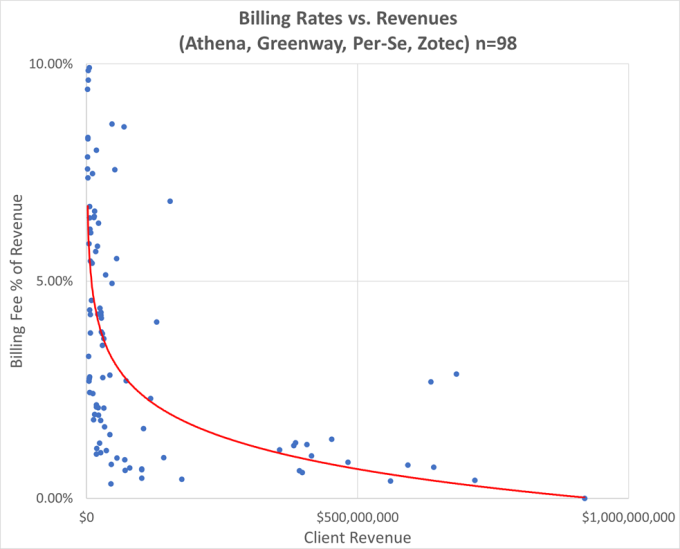

An independent practice can choose from any combination of services, including accounting, billing, payroll, staff leasing, practice management information systems, electronic health records systems, office space, equipment leasing, or supply chain management. The following charts show business management fees and revenue cycle billing rates charged by popular vendors to physician practices and ambulatory health organizations. This market data was identified in IRS Form 990 forms filed not-for-profit organizations.

Source: IRS Form 990 filings, Part VII, Section B, Independent Contractors

The pricing for each individual service on the menu is broken out and is competitive with market rates for comparable services. Practice ABC may pay 4% of collections for billing services and 1% of gross payroll for staff leasing services, while Practice XYZ may pay a flat 20% of collections for financial management, accounting, billing, staff leasing services, and information systems. Market data from sources such as IRS Form 990 filings and comparable vendor pricing can help support that individual service fees are consistent with fair market value for physician practice management services.

Comprehensive Turnkey Practice Management Services

Comprehensive turnkey practice management is simpler and cleaner. Medical and surgical professionals are employed by a professional corporation, while unlicensed support personnel, assets, facilities, equipment, and supplies are furnished by the management company.

The clean separation of professional clinical services from all other practice expenses allows for the unbundling of reimbursement into its component parts. These include Work (physician compensation), Malpractice, and Practice Expense Relative Value Units (RVUs) for each clinical professional specialty and site of service on the basis of the Resource-Based Relative Value System.

Once the subject practice specialty is identified, the appropriate ratios of practice-expenses-to-reimbursement can be calculated from public billing data. The actual utilization of codes within each specialty is used to determine the appropriate weighting of practice expense ratios. Practice expense ratios can be used as a proxy for the management fee rates for each practice specialty.

Examples: Unbundling Physician Compensation & Practice Expenses (Office-Based)

This same work-to-total RVU or practice-expense-to-total RVU approach is also commonly used to unbundle radiology professional fees in global imaging center billing arrangements. In those cases, imaging centers drop global bills for imaging services, and then unbundle facility and professional service payments when they contract with independent radiology professionals.

The key to accurately unbundling professional compensation from practice expenses is using real billing data, either from the subject practice or for similar types of physicians and advanced practice providers. This RVU-based approach is commonly used to support fair market value by isolating the practice expense component of reimbursement, rather than tying fees to physician professional income.

Fair Market Value Considerations for Physician Practice Management Fees

Establishing fair market value for physician practice management fees is critical in CPOM states and in transactions involving private equity-backed management services organizations (MSOs). Regulators are particularly sensitive to arrangements that could be interpreted as impermissible fee-splitting or disguised payments tied to physician professional revenue.

To support fair market value, organizations often rely on:

- Market-based benchmarks, including third-party vendor pricing and IRS Form 990 data

- Specialty-specific billing and reimbursement data

- RVU-based methodologies to isolate practice expense components

- Independent healthcare valuation analysis

Using these approaches helps demonstrate that management fees reflect the value of administrative and operational services—not a share of clinical income—supporting both compliance and commercial reasonableness.

LBMC’s healthcare valuation team provides fair market value opinions for physician practice management fees, including CPOM-compliant arrangements and private equity-backed MSO structures. Contact our tax and valuation advisors to get started.

Contact LBMC today to have your physician practice management arrangements reviewed.

Physician Practice Management Fee FAQs

What is fair market value for physician practice management fees?

Fair market value represents the price that would be paid for management services between independent parties in an arm’s-length transaction, consistent with market data and regulatory expectations.

Why is fair market value important in CPOM states?

In CPOM states, management fees must not resemble fee-splitting or payments tied to physician professional income. Establishing FMV helps ensure compliance with these restrictions.

How are physician practice management fees typically structured?

Fees may be structured as à la carte service pricing or comprehensive turnkey arrangements, often using fixed fees or methodologies supported by market data and RVU analysis.

Can management fees be based on a percentage of revenue?

In some cases, percentage-based fees may raise compliance concerns under CPOM and fee-splitting rules. Fixed fees or FMV-supported methodologies are often preferred.

How do RVUs support fair market value?

RVU-based methodologies help isolate practice expenses from physician compensation, allowing management fees to reflect operational costs rather than clinical revenue.

Who needs a fair market value opinion?

Healthcare organizations, MSOs, and private equity investors often require FMV opinions to support physician practice management arrangements and ensure regulatory compliance.